Fill in a Valid Massachusetts St 13 Form

Fill in a Valid Massachusetts St 13 Form

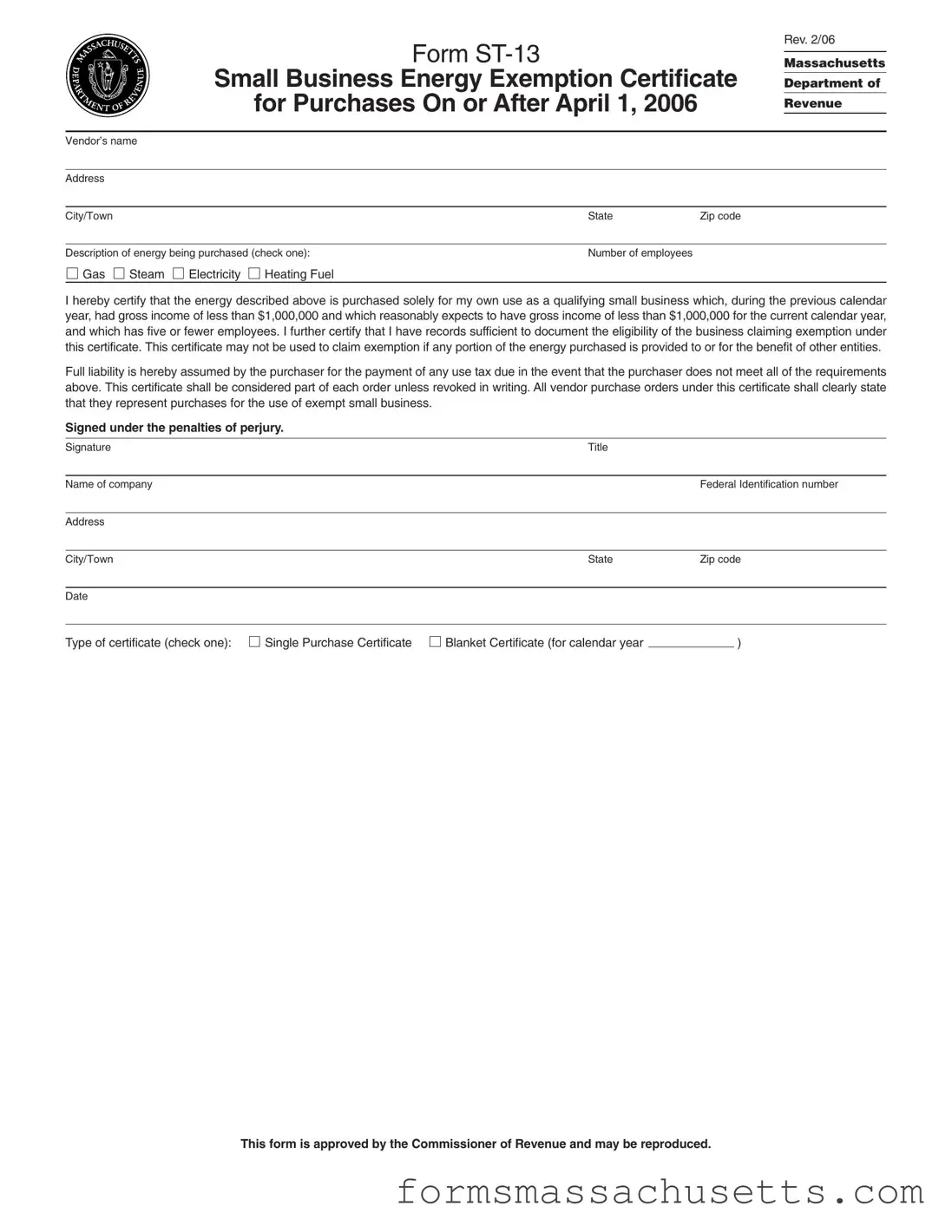

The Massachusetts ST-13 form, known as the Small Business Energy Exemption Certificate, plays a vital role for qualifying small businesses in the state. This form allows eligible businesses to purchase energy—such as gas, steam, electricity, and heating fuel—without paying sales tax, provided they meet certain criteria. To qualify, a business must have gross income of less than $1,000,000 in the previous year and reasonably expect to maintain that threshold in the current year, along with having five or fewer employees. The form requires the business to certify that the energy purchased is solely for its own use and not for the benefit of other entities. Additionally, it emphasizes the importance of maintaining proper records to document eligibility. A signed copy of the ST-13 must be presented to vendors for the exemption to apply, and businesses must ensure they comply with all requirements to avoid potential tax liabilities. This certificate not only simplifies the purchasing process for small businesses but also supports their growth by reducing operational costs associated with energy expenses.

Form

Small Business Energy Exemption Certificate

for Purchases On or After April 1, 2006

Rev. 2/06

Massachusetts

Department of

Revenue

Vendor’s name

Address

City/Town |

State |

Zip code |

|

|

|

Description of energy being purchased (check one): |

Number of employees |

|

Gas

Steam

Electricity

Heating Fuel

I hereby certify that the energy described above is purchased solely for my own use as a qualifying small business which, during the previous calendar year, had gross income of less than $1,000,000 and which reasonably expects to have gross income of less than $1,000,000 for the current calendar year, and which has five or fewer employees. I further certify that I have records sufficient to document the eligibility of the business claiming exemption under this certificate. This certificate may not be used to claim exemption if any portion of the energy purchased is provided to or for the benefit of other entities.

Full liability is hereby assumed by the purchaser for the payment of any use tax due in the event that the purchaser does not meet all of the requirements above. This certificate shall be considered part of each order unless revoked in writing. All vendor purchase orders under this certificate shall clearly state that they represent purchases for the use of exempt small business.

Signed under the penalties of perjury.

Signature |

Title |

|

|

|

|

Name of company |

|

Federal Identification number |

|

|

|

Address |

|

|

|

|

|

City/Town |

State |

Zip code |

|

|

|

Date |

|

|

Type of certificate (check one):

Single Purchase Certificate

Blanket Certificate (for calendar year |

|

) |

This form is approved by the Commissioner of Revenue and may be reproduced.

Form

General Information

All business entities with gross income of less than $1,000,000 for the previous calendar year and that reasonably expect to have gross income of less than $1,000,000 in the current calendar year, that have five or fewer employees are exempt from paying a sales tax on their purchases of gas, steam, electricity and heating fuel solely for their own use. A business that may not have had gross in- come during the preceding calendar year, such as a

Any purchaser which seeks this exemption must complete Form

Instructions to Vendors

The burden of proving that a business is entitled to the small busi- ness exemption is on the vendor unless the vendor accepts in good faith a copy of this certificate, Form

For each sale exempt from sales tax under the small business ex- emption, vendors must keep a record of the name, address, and federal identification number of the small business claiming the ex- emption, the sales price of each sale and a copy of Form

Instructions to Purchasers

A purchaser ordinarily must present this certificate to the vendor for each calendar year on or before the date of its first purchase of taxable fuel in each new calendar year. If a purchaser presents the certificate after this date, the certificate only applies to purchases made on or after the date the certificate is signed and presented to the vendor.

For purposes of this exemption, an “employee” includes any part- ner, owner or officer of the business who normally works for the business for thirty hours or more per week. Unless a taxpayer dem- onstrates otherwise, the Commissioner of Revenue will presume that any partner, owner or officer who regularly works for a business normally works for the business for thirty hours or more per week.

“Employee” also includes any other individual who is an employee as defined for federal tax withholding purposes under Internal Revenue Code (I.R.C.) Sec. 3401 and who normally works for the business for thirty hours per week or more and who is hired for a period of five months or more.

In determining number or employees, a business entity must con- sider all employees, not just employees at a particular location of the business.

If a business is a member of an affiliated group, as defined in I.R.C. Sec. 1504, all employees of all members of the group must be counted to determine whether the entire affiliated group qualifies as a small business.

The business must maintain adequate weekly employee time and wage records to substantiate any claim to this exemption.

If at any time a business that has claimed a small business exemp- tion under this certificate ceases to qualify for exemption, it must notify the vendor in writing.

A purchaser is liable for the payment of any use tax in the event that the purchaser is not eligible for the exemption.

For further information about the Small Business Energy Exemp- tion, see Massachusetts Regulation 830 CMR 64H.6.11; Technical Information Release

Warning: Willful misuse of this certificate may result in criminal tax evasion penalties of up to one year in prison and $10,000 ($50,000 for corporations) in fines.

If you have any questions about the acceptance or use of this cer- tificate, please contact the Massachusetts Department of Revenue at (617)

| Fact Name | Description |

|---|---|

| Purpose | The ST-13 form serves as a Small Business Energy Exemption Certificate, allowing qualifying small businesses to purchase energy without paying sales tax. |

| Eligibility Criteria | To qualify, a business must have gross income of less than $1,000,000 for the previous year and expect the same for the current year, with five or fewer employees. |

| Effective Date | The exemption applies to purchases made on or after April 1, 2006, provided the form is signed and presented to the vendor. |

| Vendor Requirements | Vendors must keep a record of the small business's name, address, federal identification number, sales price, and a copy of the ST-13 form for exempt sales. |

| Record Keeping | Businesses must maintain adequate records to prove eligibility, including weekly employee time and wage records. |

| Certification | The form must be signed by the purchaser, certifying that the energy is solely for the business's own use and not for other entities. |

| Revocation | The certificate remains valid until revoked in writing, and it must be presented for each calendar year. |

| Governing Laws | The use of the ST-13 form is governed by Massachusetts Regulation 830 CMR 64H.6.11 and Technical Information Release 06-2. |

Restraining Order Massachusetts - Public access to court records is generally permitted, illustrating the transparency of legal processes, with noted exceptions for privacy concerns.

For those looking to navigate the complexities of property transactions, understanding the crucial aspects of a comprehensive Real Estate Purchase Agreement is vital. This form delineates the responsibilities of both buyers and sellers to ensure a smooth process. To learn more about this important document, visit the in-depth guide on Real Estate Purchase Agreement.

Abatement Form - Instructions detail how and when to use the form to dispute various tax issues and the importance of attaching supporting documentation.