Fill in a Valid Massachusetts Abt Form

Fill in a Valid Massachusetts Abt Form

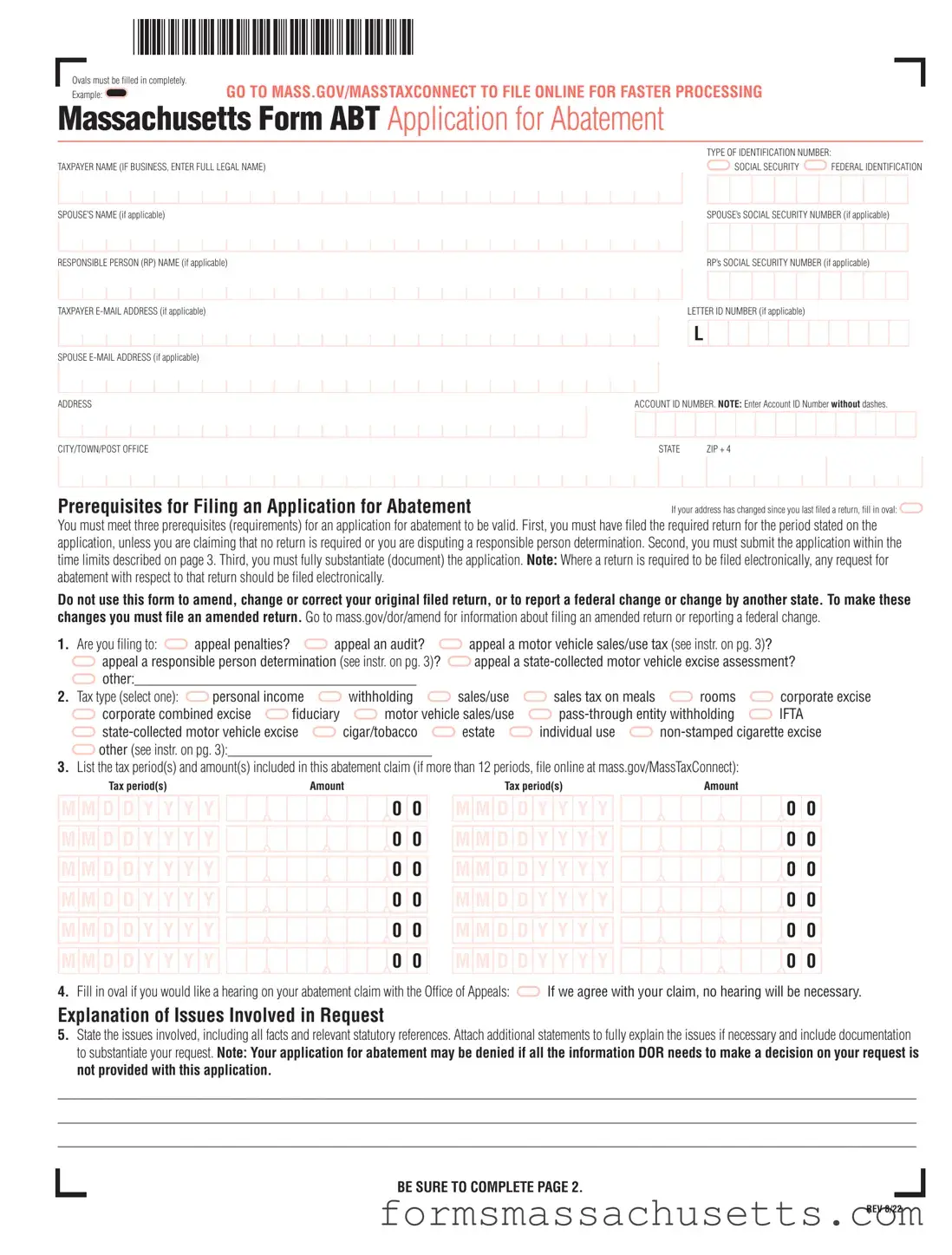

The Massachusetts Abt form, formally known as the Application for Abatement, is an essential document for taxpayers seeking to dispute tax assessments or request a reduction in their tax obligations. This form allows individuals and businesses to formally challenge various tax types, including personal income, sales and use, and corporate excise taxes, among others. To ensure a valid application, certain prerequisites must be met: the taxpayer must have filed the required return for the relevant period, fully substantiate their claims with appropriate documentation, and submit the application within specified time limits. The form requires detailed information, including taxpayer identification numbers, tax periods in question, and a clear explanation of the issues involved. Additionally, if a hearing is desired, the taxpayer can indicate this on the form. It's crucial to remember that this application cannot be used to amend a previously filed return; for such changes, an amended return must be submitted instead. Completing the form accurately and submitting it to the Massachusetts Department of Revenue is vital for those seeking relief from tax burdens.

Ovals must be filled in completely.

Example:

MASSACHUSETTS FORM ABT

TAXPAYER NAME (IF BUSINESS, ENTER FULL LEGAL NAME)

SPOUSE’S NAME (if applicable)

RESPONSIBLE PERSON (RP) NAME (if applicable)

TAXPAYER

TYPE OF IDENTIFICATION NUMBER:

SOCIAL SECURITY FEDERAL IDENTIFICATION

SPOUSE’s SOCIAL SECURITY NUMBER (if applicable)

RP’s SOCIAL SECURITY NUMBER (if applicable)

LETTER ID NUMBER (if applicable)

SPOUSE

ADDRESS |

ACCOUNT ID NUMBER. NOTE: Enter Account ID Number without dashes. |

|

CITY/TOWN/POST OFFICE |

STATE |

ZIP + 4 |

Prerequisites for Filing an Application for Abatement

If your address has changed since you last filed a return, fill in oval:

You must meet three prerequisites (requirements) for an application for abatement to be valid. First, you must have filed the required return for the period stated on the application, unless you are claiming that no return is required or you are disputing a responsible person determination. Second, you must submit the application within the time limits described on page 3. Third, you must fully substantiate (document) the application. Note: Where a return is required to be filed electronically, any request for abatement with respect to that return should be filed electronically.

Do not use this form to amend, change or correct your original filed return, or to report a federal change or change by another state. To make these changes you must file an amended return. Go to mass.gov/dor/amend for information about filing an amended return or reporting a federal change.

1. |

Are you filing to: |

appeal penalties? |

appeal an audit? |

appeal a motor vehicle sales/use tax (see instr. on pg. 3)? |

|

|||

|

appeal a responsible person determination (see instr. on pg. 3)? |

appeal a |

||||||

|

other:________________________________________ |

|

|

|

|

|||

2. |

Tax type (select one): |

personal income |

withholding |

sales/use |

sales tax on meals |

rooms |

corporate excise |

|

|

corporate combined excise |

fiduciary |

motor vehicle sales/use |

IFTA |

||||

|

cigar/tobacco |

estate |

individual use |

|||||

|

other (see instr. on pg. 3):_____________________________ |

|

|

|

|

|||

3.List the tax period(s) and amount(s) included in this abatement claim (if more than 12 periods, file online at mass.gov/MassTaxConnect):

Tax period(s) |

Amount |

Tax period(s) |

Amount |

M M D D Y Y Y Y M M D D Y Y Y Y M M D D Y Y Y Y M M D D Y Y Y Y M M D D Y Y Y Y M M D D Y Y Y Y

00

00

00

00

00

00

M M D D Y Y Y Y M M D D Y Y Y Y M M D D Y Y Y Y M M D D Y Y Y Y M M D D Y Y Y Y M M D D Y Y Y Y

00

00

00

00

00

00

4. Fill in oval if you would like a hearing on your abatement claim with the Office of Appeals: |

If we agree with your claim, no hearing will be necessary. |

Explanation of Issues Involved in Request

5.State the issues involved, including all facts and relevant statutory references. Attach additional statements to fully explain the issues if necessary and include documentation to substantiate your request. Note: Your application for abatement may be denied if all the information DOR needs to make a decision on your request is not provided with this application.

__________________________________________________________________________________________________________________________

__________________________________________________________________________________________________________________________

__________________________________________________________________________________________________________________________

BE SURE TO COMPLETE PAGE 2.

REV 8/22

FORM ABT, PAGE 2

Taxpayer or Responsible Person Consent

By filing this application for abatement, the taxpayer or responsible person gives consent for the Commissioner of Revenue to act on the application after six months from the date of filing pursuant to MGL ch 58A, § 6. You may withdraw your consent at any time. If you do not consent to allow more than six months, the application for abatement is deemed denied (1) six months from the date of filing or (2) the date consent is withdrawn, whichever is later. If you choose not to consent, fill in oval

Sign here. Under penalties of perjury, I declare that, to the best of my knowledge and belief, the information herein is true, correct and complete.

Preparer’s signature and attestation. (Fill in oval |

) I attest that I prepared this form, and that the statements contained herein, including information furnished to |

|

me by the taxpayer, are true and correct to the best of my knowledge, information and belief. |

||

Power of Attorney. (Fill in oval |

) I, the undersigned taxpayer or responsible person shown on this application, hereby appoint the following individual(s) as |

|

The

File online at mass.gov/masstaxconnect or Mail to Massachusetts Department of Revenue, PO Box 7058, Boston, MA 02204.

FORM ABT INSTRUCTIONS

Instructions

Taxpayer Information. Use a separate Form ABT for each location and account. The Letter ID number and Account ID number will help us understand your appeal. The Letter ID, beginning with L, can be found in the top

XXXrepresents three alphabet letters and the rest are digits. Note: Enter the Account ID number on Form ABT without dashes. An Account ID is required except for Motor Vehicle Sales Tax and Deeds Excise appeals.

If you are appealing a responsible person determination, see section below.

Line 1. Use this form to appeal an audit assessment; request waiver of penalties; request innocent spouse relief; challenge a responsible person determination; or request an abatement of motor vehicle excise or motor vehicle sales or use tax billed by DOR. Do not use this form to amend, change or correct your original filed return, or to report a federal change or change by another state. To make these changes you must file an amended return. Go to mass.gov/dor/amend for information about filing an amended return or reporting a federal change.

Line 2. Choose only one tax type. If appealing more than one tax type, file a separate Form ABT for each one. If your tax type is not listed, choose "Other," which includes but is not limited to alcoholic beverage excise, sales tax on telecommunication services, and

Line 3. If you have more than 12 tax periods in this abatement claim, file online at mass.gov/MassTaxConnect.

Line 5. Explain why you are requesting an abatement and attach all information necessary to support your claim. Be sure to attach Form 84, Application for Relief From Joint Income Tax Liability, if requesting innocent spouse relief. You can find guidance about appropriate documentation in DOR’s online Tax Guides at mass.gov/dor or call us at (617)

Time limits:

You must submit your application for abatement to DOR within the time limits provided in MGL ch 62C, § 37. Generally, this means:

a.Within three years from the date of the filing of the return (or within three years from the due date, if the return was filed before the due date).

b.Within two years from the date the tax was assessed or deemed to be assessed;

c.Within one year from the date the tax was paid;

d.Within two years of DOR’s determination of a responsible person’s liability;

e.Within any

Note: For an Application for Relief from Joint Income Tax Liability, review the time limits for filing under MGL ch 62C, § 84.

Additional information

To give DOR permission to discuss this application with someone other than you, complete the Power of Attorney section.

Interest and, in some cases, penalties will accrue on any unpaid amounts. Although collection activity will generally be suspended during the appeal process, you may wish to pay the amount you are appealing to stop the

accrual of interest and penalties. Note: In some cases DOR is allowed to abate penalties, but is not generally allowed to abate interest. If the abatement is approved after the assessment has been paid, a refund, with applicable interest, will be issued.

To request settlement consideration, submit Form

Important Information if Appealing Tax on a Motor Vehicle

Are you appealing the amount of sales tax paid when registering a motor vehicle?

The Registry of Motor Vehicles (RMV) and Department of Revenue (DOR) must follow Massachusetts law in determining the amount of sales tax to be paid. The amount must be the higher of the National Automobile Dealers Association (NADA) value of the vehicle as published in the Used Car Guide as “clean

When should I appeal the amount of motor vehicle sales or use tax?

If the sales tax charged was incorrectly calculated for the motor vehicle purchased or if the sales tax charged was on a motor vehicle that you believe should have been an exempt transfer or purchase. For example, if the NADA “clean

What if I think the NADA value is too high based on the condition of the car?

Massachusetts law requires the RMV to use the higher of the NADA value or the purchase price in determining the sales tax. The Department of Revenue cannot take the condition of the vehicle into account when considering an abatement request. If the NADA value is higher than the purchase price, the NADA value must be used, regardless of the vehicle’s condition. DOR will not allow a different value.

Rescission or cancellation of sale

If the abatement request is related to a rescission of sale, attach copies of:

•Bill of sale;

•Paperwork from the RMV reflecting sales tax paid, charges for the title, and registration fee;

•Registration; and

•Completed Form

Important information if appealing a responsible person determination

•Taxpayer Name – enter the responsible person’s name.

•Taxpayer ID – enter the responsible person’s Social Security number.

•Responsible Person (RP) Name and RP Social Security number – enter the responsible person’s name and Social Security number again.

•Account ID Number is the Account ID for the business tax liability for the responsible person determination.

•In Line 1, fill in the bubble for “appeal a responsible person determination.”

•In Line 2, fill in the bubble for the tax type of the business tax liability for the responsible person determination.

| Fact Name | Description |

|---|---|

| Purpose of Form | The Massachusetts Form ABT is used to apply for an abatement of various taxes, including personal income, sales/use, and motor vehicle excise taxes. |

| Prerequisites | To file a valid application, you must have filed the required return, substantiate your claim, and submit the application within specified time limits. |

| Filing Deadline | Applications must be submitted within three years of filing the return, two years from the tax assessment date, or one year from the date the tax was paid, as per MGL ch 62C, § 37. |

| Consent Requirement | By submitting the form, the taxpayer consents to allow the Commissioner of Revenue to act on the application after six months, unless consent is withdrawn. |

| Disputing Taxes | The form can be used to dispute penalties, audits, and assessments related to various tax types, including motor vehicle sales tax. |

| Submission Address | Completed applications should be mailed to the Massachusetts Department of Revenue at PO Box 7058, Boston, MA 02204. |

How Long Doesnot Take to Get a New Title for a Mobile Home in Massachusetts - Navigate the legal landscape of recreational vehicle ownership in Massachusetts through a detailed and organized titling form.

For those navigating the complexities of buying or selling property, understanding the "fundamental aspects of the Real Estate Purchase Agreement" can be vital. This document not only delineates the sale conditions but also ensures that all parties are aware of their obligations throughout the transaction. You can find a useful template and more information on the Real Estate Purchase Agreement for Colorado here.

Quarterly Fuel Tax Reporting - Emphasizes the responsibility of the applicant to ensure application completeness and accuracy.