Fill in a Valid Massachusetts 2G Form

Fill in a Valid Massachusetts 2G Form

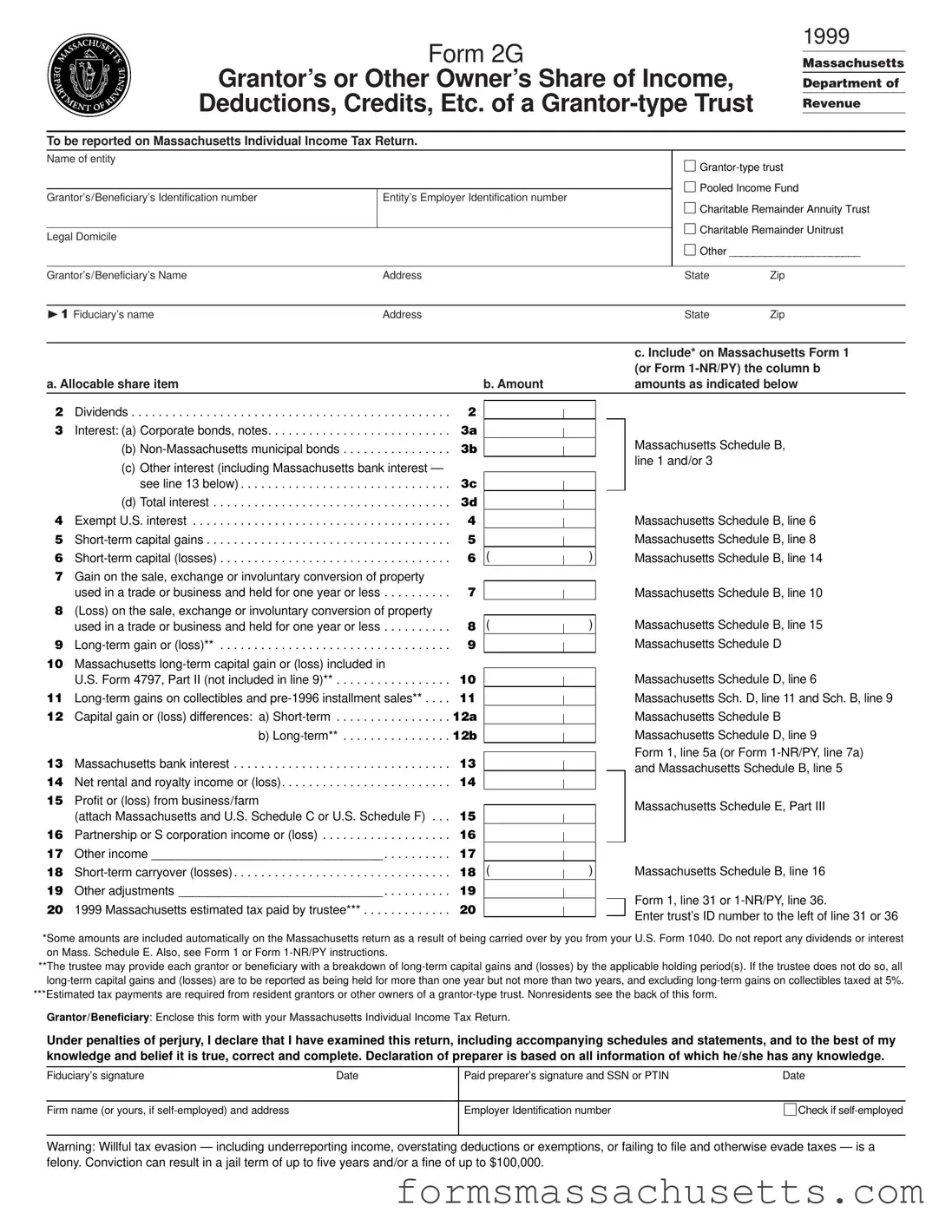

The Massachusetts 2G form, officially known as the Grantor’s or Other Owner’s Share of Income, Deductions, Credits, Etc. of a Grantor-type Trust, plays a crucial role in the tax reporting process for grantor-type trusts. This form is essential for trustees who need to report the income, deductions, and credits associated with the trust on behalf of the grantor or other owners. It requires detailed information, including the names and addresses of the trust and its fiduciary, as well as the identification numbers necessary for tax purposes. The form captures various income sources, such as dividends, interest, and capital gains, which must be accurately reported on the Massachusetts Individual Income Tax Return. Additionally, it outlines the requirements for estimated tax payments, particularly for resident grantors. The Massachusetts Department of Revenue mandates that all supporting documents, such as schedules detailing long-term capital gains or losses, be attached to ensure a complete filing. Understanding the intricacies of this form is vital for compliance and to avoid potential penalties, making it an important document for anyone involved with grantor-type trusts in Massachusetts.

Form 2G

Grantor’s or Other Owner’s Share of Income, Deductions, Credits, Etc. of a

1999

Massachusetts

Department of

Revenue

To be reported on Massachusetts Individual Income Tax Return. |

|

|

|

Name of entity |

|

||

|

|

||

|

|

Pooled Income Fund |

|

Grantor’s/Beneficiary’s Identification number |

Entity’s Employer Identification number |

|

|

|

|

Charitable Remainder Annuity Trust |

|

|

|

Charitable Remainder Unitrust |

|

Legal Domicile |

|

||

|

|

|

|

|

|

Other ______________________ |

|

|

|

|

|

Grantor’s/Beneficiary’s Name |

Address |

State |

Zip |

|

|

|

|

¨1 Fiduciary’s name |

Address |

State |

Zip |

|

|

|

|

|

|

|

|

c. Include* on Massachusetts Form 1 |

|

|

|

|

|

|

|

|

(or Form |

a. Allocable share item |

|

b. Amount |

|

|

|

|

amounts as indicated below |

|

|

|

|

|

|

|

|

|

|

2 |

Dividends |

2 |

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|||

3 |

Interest: (a) Corporate bonds, notes |

3a |

|

|

|

|

|

Massachusetts Schedule B, |

|

|

|

|

|

||||

|

(b) |

3b |

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

line 1 and/or 3 |

||

|

(c) Other interest (including Massachusetts bank interest — |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

see line 13 below) |

3c |

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

(d) Total interest |

3d |

|

|

|

|

|

Massachusetts Schedule B, line 6 |

|

|

|

|

|

|

|||

4 |

Exempt U.S. interest |

4 |

|

|

|

|

|

|

|

|

|

||||||

5 |

5 |

|

|

|

|

|

Massachusetts Schedule B, line 8 |

|

|

|

|

||||||

6 |

6 |

( |

|

) |

|

|

Massachusetts Schedule B, line 14 |

|

|

||||||||

7Gain on the sale, exchange or involuntary conversion of property

|

used in a trade or business and held for one year or less |

7 |

|

|

|

Massachusetts Schedule B, line 10 |

|

|

|

|

|||

8 |

(Loss) on the sale, exchange or involuntary conversion of property |

|

|

|

|

|

|

used in a trade or business and held for one year or less |

8 |

( |

|

) |

Massachusetts Schedule B, line 15 |

|

|

|||||

9 |

9 |

|

|

|

Massachusetts Schedule D |

|

|

|

|

10Massachusetts

|

U.S. Form 4797, Part II (not included in line 9)** |

10 |

|

|

|

|

|

Massachusetts Schedule D, line 6 |

|

|

|

|

|||||

11 |

11 |

|

|

|

|

|

Massachusetts Sch. D, line 11 and Sch. B, line 9 |

|

|

|

|

||||||

12 |

Capital gain or (loss) differences: a) |

12a |

|

|

|

|

|

Massachusetts Schedule B |

|

|

|

||||||

|

b) |

12b |

|

|

|

|

|

Massachusetts Schedule D, line 9 |

|

|

|

|

|||||

13 |

Massachusetts bank interest |

13 |

|

|

|

|

|

Form 1, line 5a (or Form |

|

|

|

||||||

|

|

|

|

|

and Massachusetts Schedule B, line 5 |

|||

14 |

. . . . . . . . . . . . . . . . . . . . . . . . .Net rental and royalty income or (loss) |

14 |

|

|

|

|

|

|

15 |

Profit or (loss) from business/farm |

|

|

|

|

|

|

Massachusetts Schedule E, Part III |

|

(attach Massachusetts and U.S. Schedule C or U.S. Schedule F) |

15 |

|

|

|

|

|

|

|

|

|

|

|

|

|

||

16 |

Partnership or S corporation income or (loss) |

16 |

|

|

|

|

|

|

|

|

|

|

|

|

|||

17 |

Other income __________________________________ |

17 |

|

|

|

|

|

|

|

|

|

|

|

|

|||

18 |

18 |

( |

|

) |

|

|

Massachusetts Schedule B, line 16 |

|

|

||||||||

19 |

Other adjustments ______________________________ |

19 |

|

|

|

|

|

Form 1, line 31 or |

|

|

|

|

|

||||

20 |

1999 Massachusetts estimated tax paid by trustee*** |

20 |

|

|

|

|

|

|

|

|

|

|

|

Enter trust’s ID number to the left of line 31 or 36 |

|||

|

|

|

|

|

|

|

|

*Some amounts are included automatically on the Massachusetts return as a result of being carried over by you from your U.S. Form 1040. Do not report any dividends or interest on Mass. Schedule E. Also, see Form 1 or Form

**The trustee may provide each grantor or beneficiary with a breakdown of

***Estimated tax payments are required from resident grantors or other owners of a

Grantor/Beneficiary: Enclose this form with your Massachusetts Individual Income Tax Return.

Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and belief it is true, correct and complete. Declaration of preparer is based on all information of which he/she has any knowledge.

Fiduciary’s signature |

Date |

Paid preparer’s signature and SSN or PTIN |

Date |

Firm name (or yours, if

Employer Identification number

Check if

Warning: Willful tax evasion — including underreporting income, overstating deductions or exemptions, or failing to file and otherwise evade taxes — is a felony. Conviction can result in a jail term of up to five years and/or a fine of up to $100,000.

Form 2G Instructions

Massachusetts has adopted the Internal Revenue Code (IRC)

Generally, a

•the trust income is distributable to/or accumulated for the ben- efit of the grantor or the grantor’s spouse;

•the grantor holds a reversionary interest in the trust which is not postponed beyond a

•the grantor has the power to revoke the trust in his/her favor;

•the grantor has the power to control the beneficial enjoyment of the trust corpus or income;

•the grantor has retained certain administrative powers with re- spect to the trust; and

•a person, other than the grantor, has the power to obtain the trust corpus or income.

Fiduciary expenses and compensation are not deductible.

All supporting details, i.e., Schedule D, if you have

The trustee may provide each grantor or beneficiary with a break- down of

Nonresident Withholding

A trustee is required to deduct and withhold from any income sub- ject to taxation (Massachusetts source income — MGL, Ch. 62, sec. 5A) at the applicable rates when the grantor or other owner is a nonresident. Form

Pooled Income Fund/Charitable Remainder Annuity or Unitrust Withholding

A Massachusetts trustee of a pooled income fund (IRC Sec, 642(c)(5)), charitable remainder annuity trust or a charitable re- mainder unitrust (IRC Sec, 664(d)), who makes payment to a Mass- achusetts beneficiary of taxable income is required to deduct and withhold tax on that income at the applicable rates. Form

Extension of Time to File

To receive an extension of time to file, you must file an Application for Extension of Time to File Fiduciary, Partnership or Corporate Trust Return, Form

Check the box for “Other” in the “Type of return filed” section on Form

Consolidated 2G Filing

If you are required to file more than one Form 2G, you can file on a “consolidated” basis. Use Form 2 as the cover for the return and complete line 1, Filing Status, in full — making sure to check the “Consolidated Form 2G” box. The signature sec- tion must also be completed and signed. Each Form 2G, or pre- approved substitute, can then be attached to the “consolidated” Form 2 without the requirement of each Form 2G being signed. Should you wish to complete lines

Due Date of Return

Form 2G is generally due on or before April 18, 2000. If filing on a fiscal year basis, the return is due on or before the 15th day of the fourth month after the close of the fiscal year.

Mail Form 2G to:

Massachusetts Department of Revenue

PO Box 7017

Boston, MA 02204

Direct fiduciary inquiries, not returns, to:

Massachusetts Department of Revenue

Customer Service Bureau

PO Box 7010

Boston, MA 02204

Telephone: (617)

| Fact Name | Details |

|---|---|

| Purpose of Form 2G | Form 2G is used to report a grantor's or other owner's share of income, deductions, and credits from a grantor-type trust on their Massachusetts Individual Income Tax Return. |

| Governing Laws | This form is governed by the Internal Revenue Code (IRC) grantor-type trust rules found in IRC Sections 671-678 and Massachusetts General Laws (MGL), Chapter 62, Section 10. |

| Filing Requirements | The trustee must file Form 2G and provide a copy to the grantor or owner, who must then report the trust income on their individual tax return. |

| Due Date | Form 2G is generally due on or before April 18 of the year following the tax year. For fiscal year filers, it is due on the 15th day of the fourth month after the fiscal year ends. |

Is There Sales Tax in Massachusetts - By completing and submitting the ST-6 form, taxpayers contribute to the responsible and lawful commerce within Massachusetts.

For those in need of a reliable form, the printable Hold Harmless Agreement template is a crucial resource. This document plays a vital role in shielding individuals from liability, making it particularly valuable for various activities requiring a waiver of responsibility. You can find a comprehensive version of this form at this printable Hold Harmless Agreement.

Withholding Tax Form M-941 - Providing accurate employee and withholding information is vital for the proper allocation of funds to state tax collections.